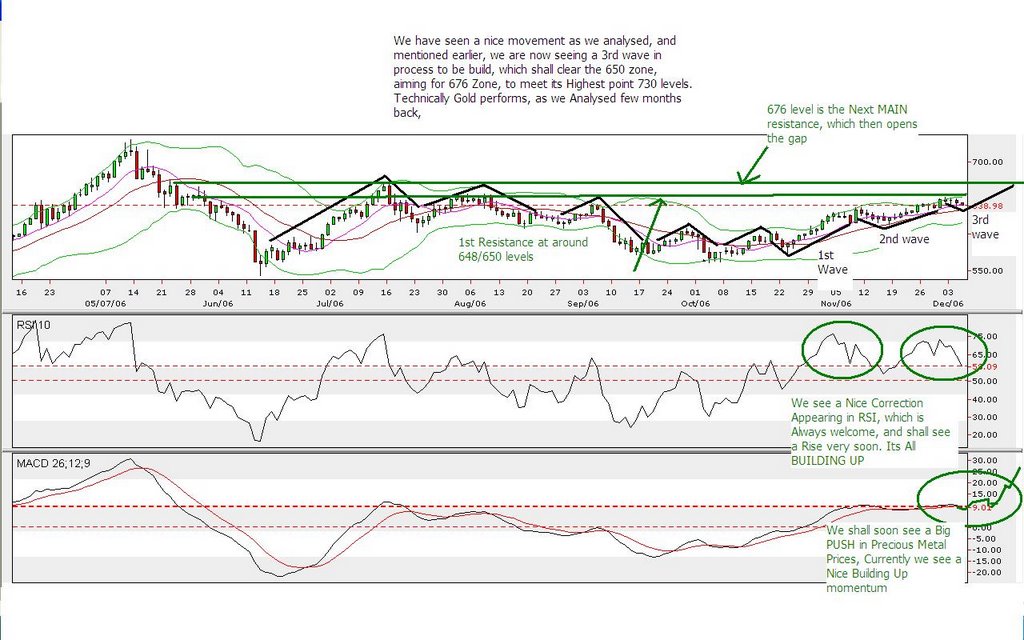

FOREX EUROPE UPDATE - USD

0 Comments for:

The USD was slightly lower amid a quiet session overnight in Asia after Thursday's swings, trading in a 1.3133-1.3175 range against the EUR and a 118.74-119.05 range against the JPY.

The dollar rallied yesterday as US consumer confidence hit an eight-month high, while existing home sales and Chicago PMI also came in stronger-than expected and initial claims were basically in line with consensus.

The greenback had initially suffered ahead of the North American open as ECB governing board member Yves Mersch said that Eurozone rates remained too low and policy was accommodative.

The strong data indicated improved economic activity over the holiday period and continues to ask questions on the Fed's rate outlook for next year. The implied yield on the Dec 07 Euro$ contract has gained 16.5 bp since markets returned from Christmas holidays.

However, while optimism on the US economy is on the rise after a string of positive data during recent sessions, the dollar has not strengthened sharply, indicating the market remains cautious over the economic and rate outlook for next year.

On the housing market front, our economists note that while home sales may be in the process of stabilising as prices have become more attractive, the consumer spending fallout from the abundance of unsold homes and lower prices is likely to spill over into other areas of the economy-a key risk to the dollar in the medium term.

Despite a pickup in the Chicago PMI, recent manufacturing surveys have shown broader weakness in the sector and the shadow of a weakening labour market continues to loom. Next week's non-farm payrolls data could set an early pace for the dollar's 2007 performance as the market begins to turn its attention towards broader US and global growth prospects and also the timing of potential of Fed easing.

The dollar has benefited from risk-sentiment by investors throughout the second half of 2006 and any reversal in 2007, especially if a global slowdown story comes into the fray, will pose another threat to the dollar's current resilience.

Ahead today, there are no important releases of note, and as today is the final trading day of 2006, A very happy new year to All.

posted by GoldTrade @ 2:06 AM

0 comments

![]()

![]()